Why does a lender need a profit and loss statement?

Rachel Acosta

Rachel Acosta

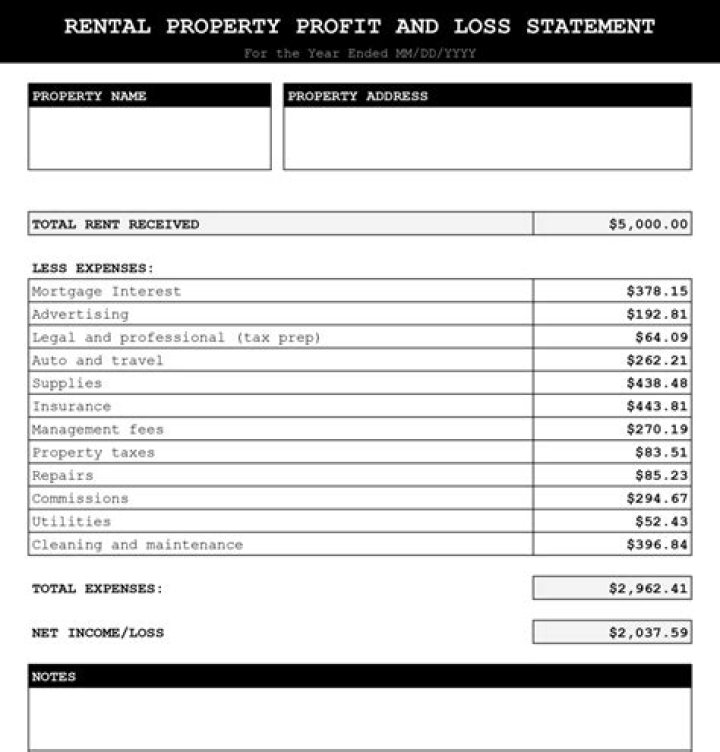

This statement shows revenues and expenses of the business, and resulting profit or loss, over a specific time period (a month, a quarter, or a year). Reviewing the profit and loss statement helps the business make decisions and to prepare the business tax return.

How do you prepare a profit/loss statement?

How to write a profit and loss statement

- Step 1: Calculate revenue.

- Step 2: Calculate cost of goods sold.

- Step 3: Subtract cost of goods sold from revenue to determine gross profit.

- Step 4: Calculate operating expenses.

- Step 5: Subtract operating expenses from gross profit to obtain operating profit.

How do you prepare a simple profit and loss statement?

How are profit and loss statements used in the mortgage business?

How are profit and loss statements used in the mortgage business? The main purpose of a profit and loss is to confirm filed business income with the IRS is stable or increasing since the last tax filing. Depending on what agency you use, this could be a short as one quarter since filing (for FHA loans).

How often should you review your profit and loss statement?

Every business should prepare and review its profit and loss statement periodically – at least every quarter. Reviewing the profit and loss statement helps the business make decisions and to prepare the business tax return.

How does a loss on a business affect your mortgage?

If a borrower who owns a stake in a business submits a corporate tax return that reflects a loss for that business in the previous tax year, that loss could reflect negatively on that person’s individual salary reported as part of his or her mortgage application.

How to write a profit or loss statement?

Write a list of those expenses such as “Gas”, “Materials”, “Legal Expenses”, etc. and then show your total income from that job or “contract” subtract the expenses and show your total profit or loss hence Profit / Loss Statement.