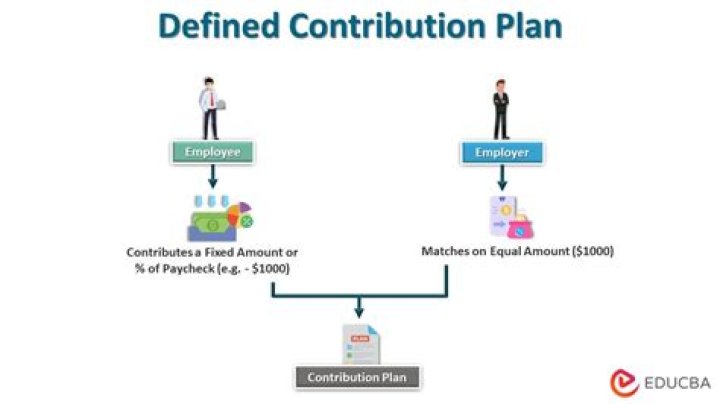

Who can contribute to a defined contribution plan?

Mia Horton

Mia Horton

In a defined contribution plan, both you and your employer can contribute to your individual account. For some plans, you may be required to wait up to one year before enrolling.

Can a self-employed person have a defined benefit plan?

Self-Employed Defined Benefit Plans Allow Large Tax-Deductible Contributions. If you are self-employed, a Defined Benefit Plan significantly reduces your taxes WHILE you save for your OWN retirement. By contrast, someone who is self-employed may contribute $100,000 to $250,000+ per year in a Defined Benefit Plan.

Can employees contribute to a defined benefit plan?

Employers are normally the only contributors to the plan. But defined benefit plans can require that employees contribute to the plan. You may have to work for a specific number of years before you have a permanent right to any retirement benefit under a plan.

How much can an employer contribute to a defined benefit plan?

Under 2006 Pension Protection Act legislation, your business can make employer contributions to a defined contribution plan of up to 6% of compensation (with each employee’s compensation capped at the IRS limit).

What is better defined benefit or defined contribution?

A Better Bang for the Buck: The Economic Efficiencies of DB Plans. This report finds that a defined benefit (DB) pension plan can deliver the same level of retirement income to a group of employees at 46% lower cost than an individual defined contribution (DC) account.

Can a company contribute to a defined contribution plan?

Employer-sponsored defined-contribution plans may also receive matching contributions. More than three-fourths of companies contribute to employee 401 (k) accounts based on the amount the participant contributes.

Do you have to contribute to company retirement plan?

There are no matching contributions, no shares of company stock, and no automatic payroll deductions. You’ll have to be highly disciplined in contributing to the plan and, because the amount you can put in your retirement accounts depends on how much you earn, you won’t really know until the end of the year how much you can contribute.

Is the Thrift Savings Plan a defined contribution plan?

The Thrift Savings Plan is used for federal government employees, while 529 plans are used to fund a child’s college education. Since individual retirement accounts often entail defined contributions into tax-advantaged accounts with no concrete benefits, they could also be considered a defined-contribution plan.

What are defined benefit plans for business owners?

Defined benefit plans are a class of pension plans sponsored by an employer that can give the largest possible benefit to the participants. They are an ideal solution for someone who is a business owner or a self-employed individual as it can help save for retirement while lowering taxable income.