When reporting a change in accounting principle required disclosures on the income statement include?

David Mack

David Mack

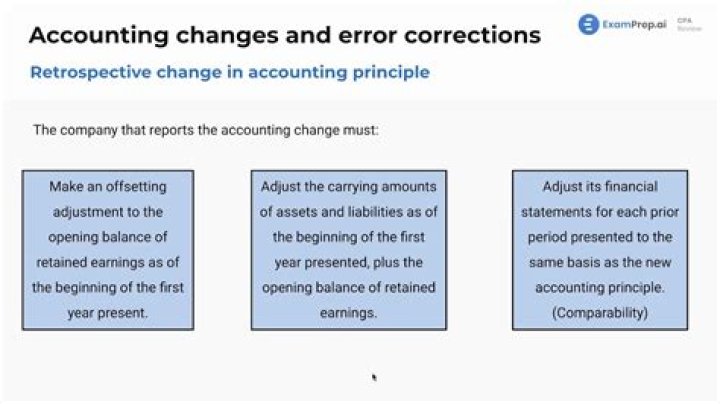

154, the required disclosures for a change in principle include a description of the change and the reason for it, as well as an explanation of why the newly adopted principle is preferable.

When companies make changes that result in different reporting entities The change is reported prospectively?

Terms in this set (20) When a company changes an accounting principle, it should report the change by reporting the cumulative effect of the change in the current year’s income statement.

What disclosures are required for an accounting principle change?

An entity is required to disclose the impact of the change in accounting estimates on its income from continuing operations, net income (including per share amounts) of the current period.

Which is the reason why entities are permitted to change accounting policy?

A common reason why an entity voluntarily changes an accounting policy is to reflect explanatory material included in agenda decisions published by the IFRS Interpretations Committee (agenda decisions).

What is a change in accounting principles?

A change in accounting principle is the term used when a business selects between different generally accepted accounting principles or changes the method with which a principle is applied. Accounting principles impact the methods used, whereas an estimate refers to a specific recalculation.

What happens when you make a change in estimate?

A change in accounting estimate is an adjustment of the carrying amount of an asset or liability, or related expense, resulting from reassessing the expected future benefits and obligations associated with that asset or liability.

How do you account for change in useful life?

As we can see from this example, the change in the useful life estimate affects:

- Balance sheet: depreciation expense => accumulated depreciation => fixed asset book value.

- Income statement: depreciation expense => net income.