When an auditor issues an adverse report he or she must use the term?

William Clark

William Clark

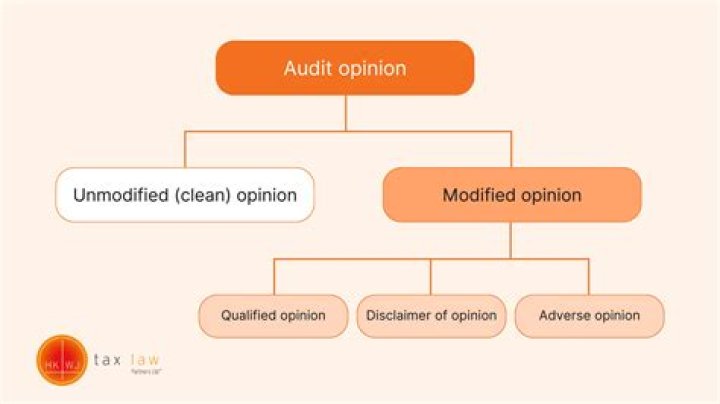

Whenever an auditor issues a qualified report, he or she must use the term “subject to” in the opinion paragraph. When there is a scope limitation in an audit, the audit report will be unqualified, qualified scope and opinion, or adverse, depending on the materiality of the scope limitation.

What is adverse opinion in auditing environment?

An adverse opinion is a statement made by an entity’s outside auditor, that the entity’s financial statements do not fairly represent its results, financial position, and cash flows. The auditor states the reason for this type of opinion within the report.

What is difference between qualified opinion and adverse opinion?

A qualified opinion is a reflection of the auditor’s inability to give an unqualified, or clean, audit opinion. The adverse opinion results in the company needing to restate and complete another audit of its financial statements. A qualified opinion is still acceptable to most lenders, creditors, and investors.

What is adverse of opinion?

An adverse opinion is a professional opinion made by an auditor indicating that a company’s financial statements are misrepresented, misstated, and do not accurately reflect its financial performance and health.

What is an unqualified opinion?

What Is an Unqualified Opinion? An unqualified opinion is an independent auditor’s judgment that a company’s financial statements are fairly and appropriately presented, without any identified exceptions, and in compliance with generally accepted accounting principles (GAAP).

What is an adverse opinion?

Is adverse opinion bad?

Qualified opinions are generally bad news, but not necessarily fatal to a company. There are two types of negative audit reports. The first is an adverse opinion, meaning the financial statements are materially misstated. In such a case the company needs a new independent auditor.

Is going concern a qualified opinion?

What does an audit opinion mean? When uncertainties exist regarding the going concern assumption, the auditor will typically issue a “qualified” opinion and disclose the nature of these uncertainties in the footnotes.

When to issue a qualified or adverse opinion?

A qualified or adverse opinion must be issued when the auditor knows the financial statements may be misleading because they were not prepared in conformity with GAAP (depending on materiality). The opinion must state the nature of the deviation from GAAP and the amount of the misstatement.

What are the different types of adverse opinions?

An adverse opinion is one of the four main types of opinions that an auditor can issue. The other three are unqualified opinion, which means that financial statements are presented in accordance with GAAP; qualified opinion, which means that there are some material misstatements or misrepresentations but no evidence of systemic non-compliance …

When to obtain an adverse audit opinion from IFAC?

If the misstatements are material and pervasive, the adverse opinion should be issued. If the auditor could not obtain evidence and the items that auditors could not obtain could be material and pervasive, disclaimer opinion should be obtained. The following is the example of Adverse Audit Opinion from IFAC:

What does an auditor’s adverse opinion mean to investors?

Thirdly, an “adverse” opinion means the auditor finds one or both of the following. Statements do no t fairly represent the entity’s accounts. The audited statements do not comply with GAAP.