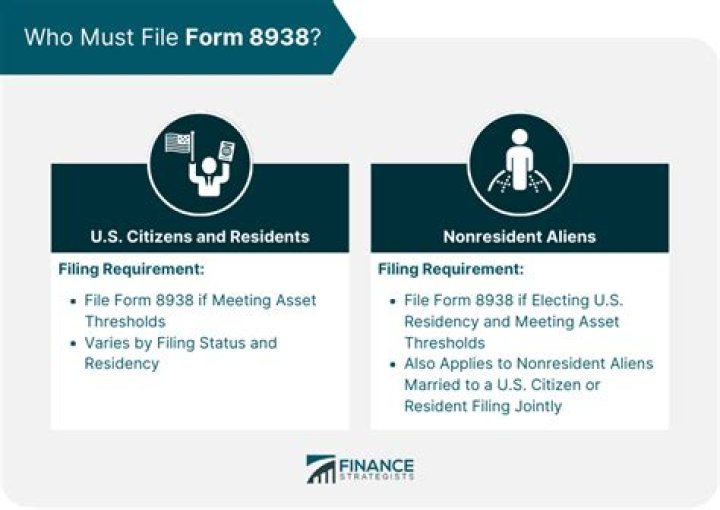

What must be reported on Form 8938?

David Mack

David Mack

More In File Certain U.S. taxpayers holding specified foreign financial assets with an aggregate value exceeding $50,000 will report information about those assets on new Form 8938, which must be attached to the taxpayer’s annual income tax return.

What is a specified domestic entity Form 8938?

Certain domestic corporations, partnerships, and trusts that are considered formed or availed of for the purpose of holding, directly or indirectly, specified foreign financial assets (specified domestic entities) must file Form 8938 if the total value of those assets exceeds $50,000 on the last day of the tax year or …

Does a trust file an FBAR?

The trust is a United States person because it is organized under California law. The trust must therefore report the account on its FBAR, even though it does not have its own EIN and does not have any obligation to file its own income tax return.

Who must file Form 8939?

Unmarried individuals residing in the United States are required to file Form 8938 if the market value of their foreign financial assets is greater than $50,000 on the last day of the year or greater than $75,000 at any time during the year.

Are distributions from foreign trusts taxable?

In contrast, income from a foreign nongrantor trust is generally taxed when distributed to U.S. beneficiaries, except to the extent U.S. source or effectively connected income is earned and retained by the trust, in which case the nongrantor trust would pay U.S. income tax for the year such income is earned.

What should be included in a grantor trust Form 1041?

The general rule, found in IRC Reg §1.671-4 (a), is that all grantor trusts must file a Form 1041, which contains only the trust’s name, address, and tax identification number (TIN).

When does a nongrantor trust need to file Form 8938?

A domestic nongrantor trust must file Form 8938 with Form 1041 for years that begin in 2016 or later if both of the following are true: The trust directly holds specified foreign financial assets having an aggregate value exceeding $50,000 on the last day of the entity’s taxable year or $75,000 at any time during the entity’s taxable year.

Where does a grantor trust report its income?

The tax return filing provides the IRS notice that although the grantor trust has it’s own tax ID number, the income and related trust expenses are reported on the grantor’s federal tax return.

Do you have to file a foreign grantor trust statement?

The trustee must also send a “Foreign Grantor Trust Owner Statement” to each U.S. owner of a portion of the trust and a “Foreign Grantor Trust Beneficiary Statement” to each U.S. beneficiary who received a distribution during the taxable year. If the trustee does not file Form 3520-A as required, penalties are imposed on the U.S. grantor.