What is the journal entry for restricted cash?

William Clark

William Clark

The journal entry is to debit a “Release of Restriction — Temporarily Restricted” account and credit “Release of Restriction — Unrestricted” account. Note that the revenue account is not touched when revenues are released — release accounts are used instead.

When should donor restricted contributions be recognized as revenue?

A restriction by a donor can impact the timing of revenue recognition, since it can only be revenue if the contribution is an unconditional transfer to the not-for-profit. Only after a conditional transfer becomes unconditional can it be recognized as revenue.

Where is restricted cash reported on the balance sheet?

If it is not expected to be used within a one-year time frame, it is classified as a non-current asset. Restricted cash typically appears on a company’s balance sheet as either “other restricted cash” or as “other assets.”

Is Restricted cash a debit or credit?

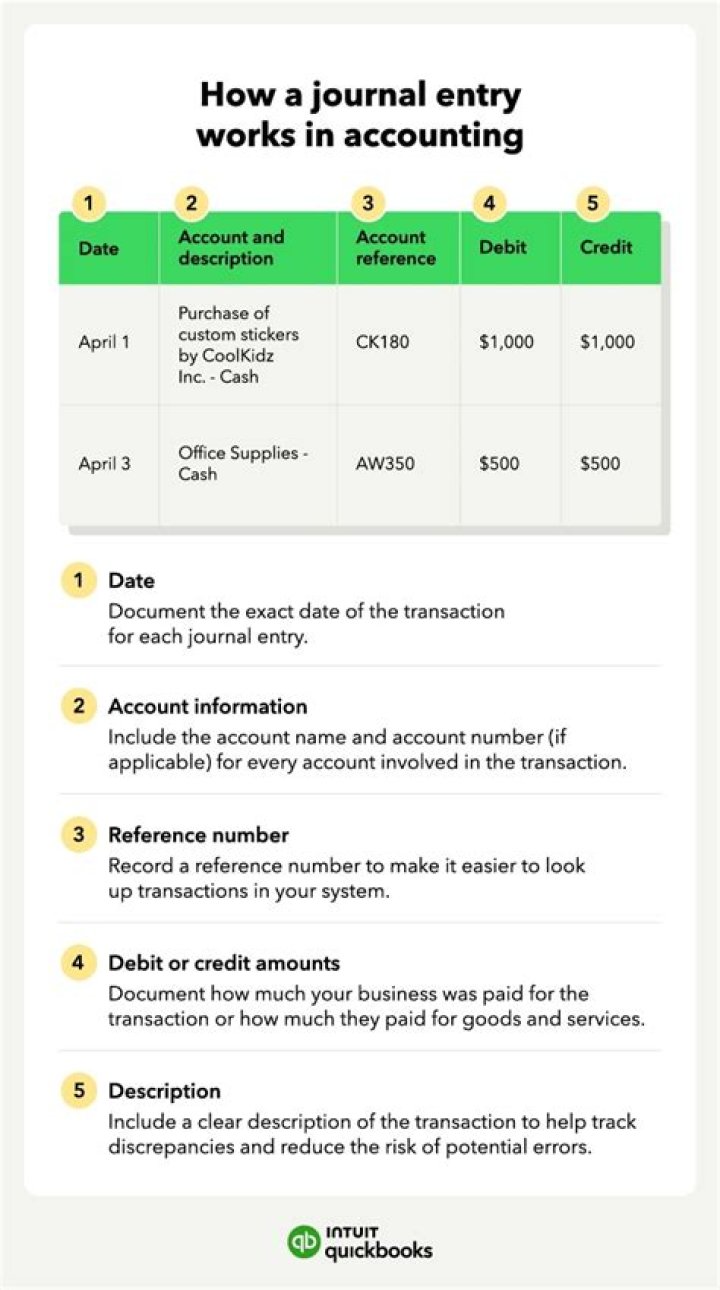

Restricted Fund Accounting Journal Entries When dealing with an asset account, a debit will increase the account balance. Therefore, completing the journal entry requires a debit to the restricted fund account for $10,000.

What are the accounting requirements for restricted funds?

Once a contribution or grant is identified as restricted, the accounting and recordkeeping requirements are of paramount importance. Two principles are at the core of the accounting requirements. First, restrictions are imposed by the donor when they make the gift or grant.

How to account for restricted and unrestricted funding?

The accounting requirements for restricted funds can be managed in a few different ways, depending on the accounting software being used and the sophistication of the chart of accounts. The most effective practice is to display grants and contributions with donor restrictions in a separate column.

What can a nonprofit do with a donor restricted contribution?

A donor may, for instance, request that their funds be kept as an investment for the next ten years. The nonprofit must track how long those funds have been held so that, after the ten-year period has passed, they can transfer those assets over to the assets without donor restrictions section of the financials and use those funds freely.

How are restricted funds recorded on a nonprofit’s books?

Budgeting will be separate, so will expensing, and other aspects of the accounting process. All of the income from restricted funds, including multi-year grants, are expected to be recorded on the nonprofit’s books in the year an irrevocable commitment to the funding was received.