What is the journal entry for acquisition?

Matthew Wilson

Matthew Wilson

To record an acquisition using the fair market value of assets and liabilities, with an entry to goodwill that records the difference between this total and the price paid. To record the offsetting of negative goodwill against accounts that do not have to be carried at fair value.

What are the accounting entries to record?

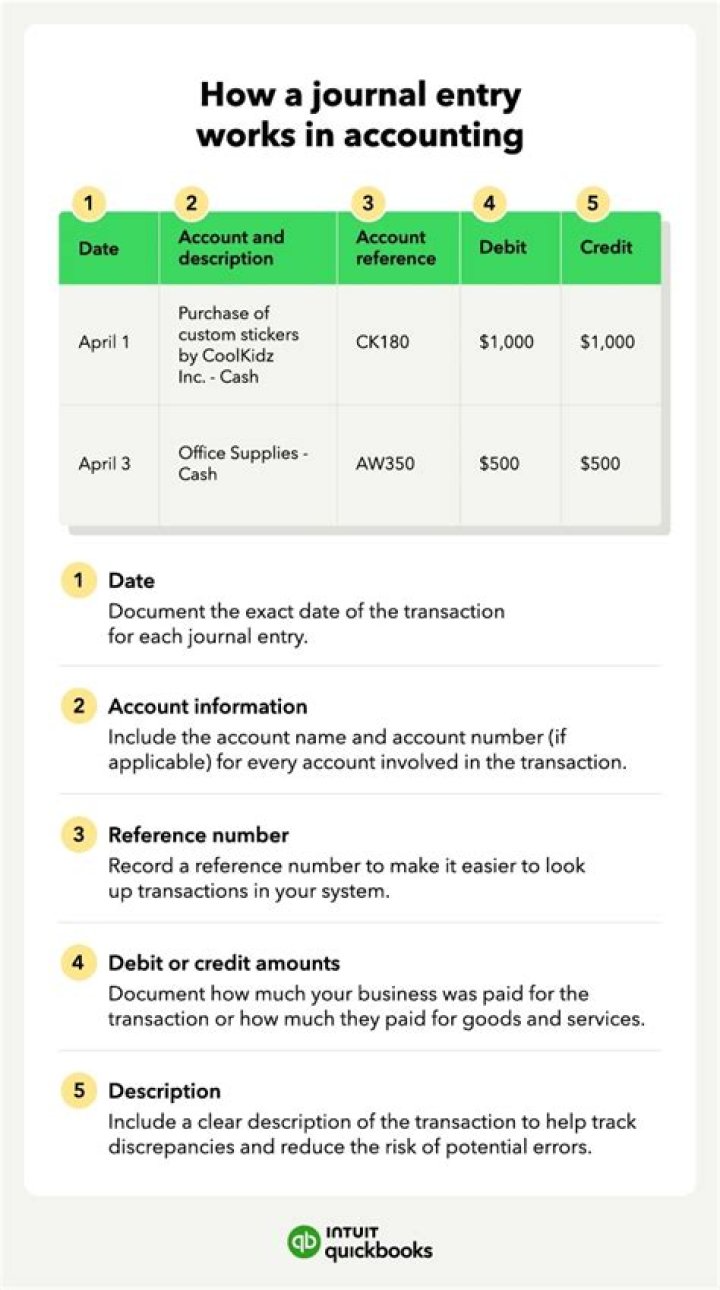

A journal entry is a record of the business transactions in the accounting books of a business. A properly documented journal entry consists of the correct date, amounts to be debited and credited, description of the transaction and a unique reference number. A journal entry is the first step in the accounting cycle.

How do acquisitions affect balance sheet?

Under standard accounting rules, any costs you incurred to carry out the acquisition are considered part of the purchase price, according to Corporate Finance Institute. As such, they go on the balance sheet as capitalized costs, not on the income statement as expenses.

Where do acquisitions go in the balance sheet?

Where do acquisitions go on balance sheet?

Acquisition cost is placed on a company’s balance sheet under the fixed assets section. The total cost included on the balance sheet will include all costs incurred to use the asset, including costs associated with getting the asset working and producing.

What are the basic accounting entries?

The Ten Most Common Journal Entries

- Journal Entry for the Owner Investing Capital.

- Journal Entry for a Liability (Debt)

- Journal Entry for Purchasing an Asset.

- Journal Entry for Withdrawing Owner’s Funds.

- Journal Entry for Cash Income.

- Journal Entry for Income on Credit.

- Journal Entry for Receiving Money from a Debtor.

What is the journal entry to record an acquisition?

What is the journal entry to record an acquisition? When a company acquires more than 50% of another company, US GAAP requires the acquirer to consolidate the acquired company under the consolidation method. The visual below illustrates the 6-step process that can be used to record a journal entry on the acquisition date:

How is the purchase price recorded in acquisition accounting?

In an acquisition, the purchase price becomes the target co’s new equity. The excess of the purchase price over the FMV of the equity (assets – liabilities is captured as an asset called goodwill. Under purchase accounting, the purchase price is first allocated to the book values of the assets, net of liabilities.

When does a journal entry need to be reversed?

There are a few instances where journal entries should be reversed in the following accounting period. When this is necessary, a warning note is attached to the bottom of the relevant journal entries. B.1 ACQUISITIONS To record an acquisition using the fair market value of assets and liabilities, with an entry

What is the journal entry for investment in subsidiary?

If 100% share capital of an entity is owned by the parent company then such an entity will be referred to as wholly-owned subsidiary. The parent company will report the “investment in subsidiary” as an asset in its balance sheet. Whereas, the subsidiary company will report the same transaction as “equity” in its balance sheet.