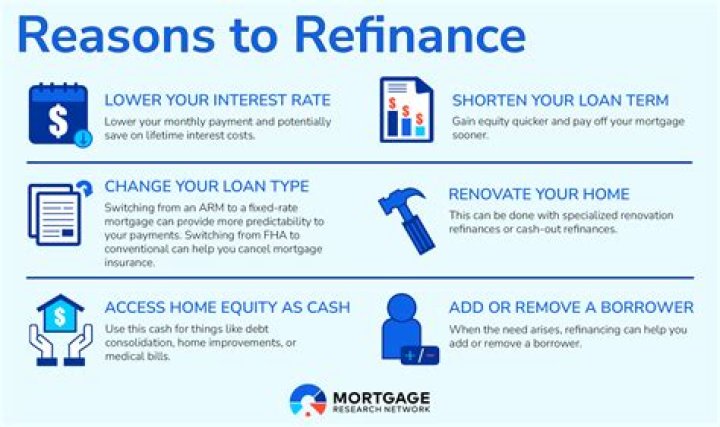

What is the best scenario for refinancing a mortgage?

Rachel Acosta

Rachel Acosta

When it’s a good idea to refinance your mortgage Consider refinancing if you can lower your interest rate by one-half to three-quarters of a percentage point — this can substantially lower your monthly payment. Make sure your total monthly savings offset the cost of refinancing, however.

Why would you be denied a refinance?

The most common reason why refinance loan applications are denied is that the borrower has too much debt. Because lenders have to make a good-faith effort to ensure you can repay your loan, they typically have limits on what’s called your debt-to-income (DTI) ratio. Ideally, your DTI ratio should be 36% or lower.

Is it hard to get approved for refinance?

Just like with your original mortgage, the higher your credit score, the better your rate. Most lenders require a credit score of 620 in order to refinance to a conventional loan. If you have a conventional loan, you have to qualify as if you were purchasing the home for the first time.

What should I do if I want to refinance my mortgage?

Do a break-even analysis to see if refinancing is something worth doing in your situation. That just means running the numbers to see if you’ll be in your home long enough to benefit from the savings that a lower interest rate and payment could bring.

What happens if I refinance with a different bank?

If you go with a different bank to refi your first mortgage, you’ll need to get your current mortgage company to subordinate the second mortgage. This just means that the holder of the second mortgage agrees that the new bank refinancing the first mortgage has first dibs on your home should you default on the loan.

Do you have to pay PMI when refinancing your home?

If for some reason your home has dropped in value, refinancing your home can tack on extra costs, such as private mortgage insurance. Borrowers with small down payments — or refinances with little equity — have to pay PMI until their equity reaches 20% of the home’s value.

When to refinance a 30 year fixed rate mortgage?

The Length of Your Mortgage Is Over 15 Years If your original mortgage is a 30-year term (or more), then refinancing is a good way to get to the ultimate goal of locking in a 15-year fixed-rate mortgage —ideally with a new payment that’s no more than 25% of your take-home pay.