What is IRS tax form 4972?

William Clark

William Clark

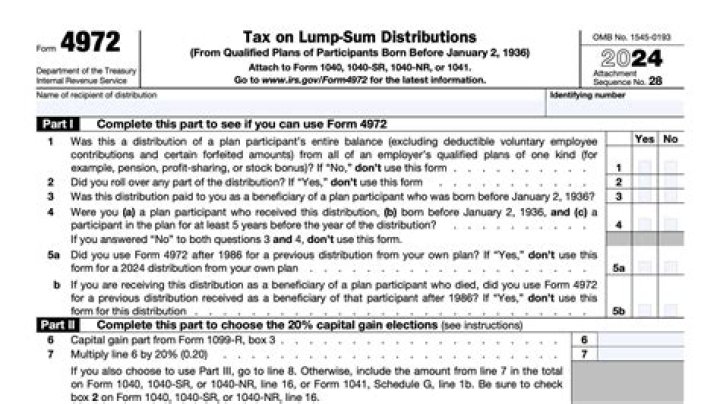

Use Form 4972 to figure the tax on a qualified lump-sum distribution (defined below) you received in 2020 using the 20% capital gain election, the 10-year tax option, or both.

What is the purpose of Form 4972?

A form that one files with the IRS to calculate and pay the tax owed on lump-sum distributions from qualified retirement plans. Filing this form may result in paying lower taxes on the distribution than one would if it were taxed as ordinary income.

How do I report a lump-sum distribution?

Assuming you qualify, the IRS allows you to elect one of five methods of taxation for lump-sum distributions:

- Report part of your withdrawal as a capital gain, with the remainder being ordinary income;

- Report part of your withdrawal as a capital gain, and use the 10-year tax option for the remainder;

Is a lump sum payment taxable?

Under current tax law, both your employer and member benefits may be subject to tax if withdrawn as either a rollover or cash lump sum. The only exception to this is dependant payments made in the case of a member’s death. You pay no money on the tax–free component when you claim your benefit.

What do you need to know about form 4972?

However, IRS Form 4972 allows you to claim preferential tax treatment if you meet a series of special requirements. The biggest requirement is that you have to be born before January 2, 1936. Taking a lump-sum distribution Retirement plans are intended to provide you with income after you stop working.

How are distributions from a deceased mother’s Ira taxable?

1 Inherited Basis. When you inherit your mother’s IRA, you take her basis in the account. 2 Traditional IRA Distributions. Distributions from a traditional IRA inherited from your mother are fully taxable unless she made nondeductible contributions to the account. 3 Roth IRA Distributions. 4 No Penalties. …

What do I have to do as a beneficiary of an IRA?

Beneficiaries of a retirement account or traditional IRA must include in their gross income any taxable distributions they receive.

Can a deceased spouse’s IRA be rolled over to a living spouse?

If a surviving spouse receives a distribution from his or her deceased spouse’s IRA, it can be rolled over into an IRA of the surviving spouse within the 60-day time limit, as long as the distribution is not a required distribution, even if the surviving spouse is not the sole beneficiary of his or her deceased spouse’s IRA.