What does Section 125 of the IRS Code allow employers to do?

Isabella Ramos

Isabella Ramos

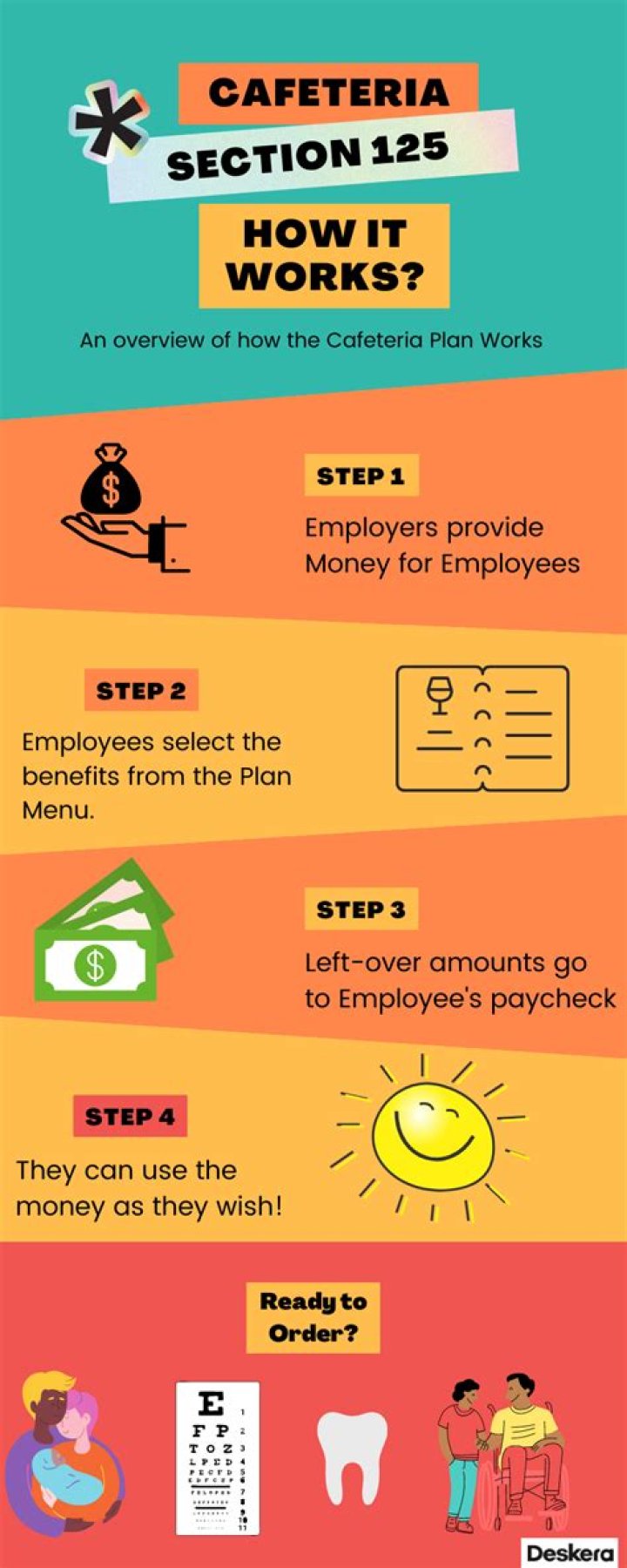

Code Section 125 allows employers to establish a type of tax savings arrangement, called a Section 125 plan or cafeteria plan, for their employees. A Section 125 plan provides employees with an opportunity to pay for certain benefits on a pre-tax basis, allowing them to increase their take-home pay.

When should I update my Section 125 plan document?

Section 125 of the Internal Revenue Code (the Code) requires that Premium Only or Cafeteria plan documents be updated every five years. Section 125 plan documents also need to be restated whenever there is a change in your plan or in the law governing the plan.

Who sets up a Section 125 plan?

Section 125 cafeteria plans must be created by an employer. Once a plan is created, the benefits are available to employees, their spouses, and dependents. Depending on the circumstances and details of the plan, Section 125 benefits may also extend to former employees, but the plan cannot exist primarily for them.

What are the requirements for a Section 125 plan?

A Section 125 Plan must offer a choice between at least one taxable benefit (such as salary) and one qualified benefit (such as major medical coverage). A plan that does not offer this choice is not a Section 125 Plan and may be disqualified by the Internal Revenue Service (IRS) in the event of an audit.

Can I write my own Section 125 plan?

Section 125 of the Code clearly states that “a written plan” is required as part of a Cafeteria Plan that allows employees to choose to participate in a plan with qualified benefits. Therefore, tax-advantage treatment of employee group benefits is not allowed without a written plan document in place.

What are considered Section 125 deductions?

In a section 125 plan or cafeteria plan, employees can pay qualified medical, dental, or dependent-care expenses on a pretax basis, which has the effect of reducing their taxable income as well as their employer’s Social Security (FICA) liability, federal income and unemployment taxes, and state unemployment taxes …

Is Section 125 Mandatory?

Income tax savings for the employee: A Sec. 125 plan is required for employers who want to allow employees to choose the qualified benefits they want and avoid paying income taxes on the amount of wages they contribute to obtain those benefits.

What benefits are included in section 125?

Is Section 125 required?

125 plan is required for employers who want to allow employees to choose the qualified benefits they want and avoid paying income taxes on the amount of wages they contribute to obtain those benefits. Flexible spending account (FSA) benefits for the employee: FSAs can only be offered through a Sec. 125 plan.

Can a small employer file a section 125 plan?

Section 125 of the IRS Code requires an employer have a written plan document in place whether the plan covers 1 or 100,000 employees. Setting up a Section 125 plan for small employers is a lot of paperwork for just one employee. Not at all. It’s as easy as sign, copy, and file.

What do you need to know about Section 125?

IRS Forms Needed to Implement a Section 125 Plan. A Section 125 plan is called a cafeteria plan. This plan allows employees to choose to withhold pre-tax salary to cover the cost of specific benefits, or to choose between taxable and non-taxable.

How many employees are exempt from Section 125?

Since employers with fewer than 50 employees are exempt from the ACA mandate they are also exempt from the requirement for a written Section 125 plan document. Section 125 of the IRS Code requires an employer have a written plan document in place whether the plan covers 1 or 100,000 employees.

Can a cafeteria plan be part of a section 125 plan?

A Section 125 plan must give employees a choice between taxable and non-taxable benefits. A written plan that only contains taxable benefits is not eligible for cafeteria plan benefits.