What does Notice of Federal Tax lien mean?

Matthew Wilson

Matthew Wilson

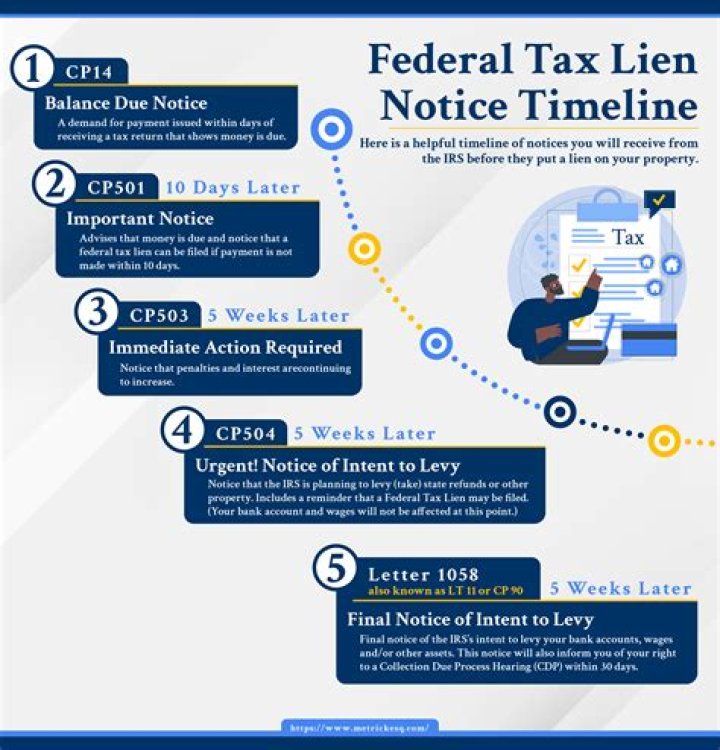

The IRS files a public document, the Notice of Federal Tax Lien, to alert creditors that the government has a legal right to your property. When filed, the Notice of Federal Tax Lien is a public document that alerts other creditors that the IRS is asserting a secured claim against your assets.

What happens if the IRS puts a lien on your house?

Normally, if you have equity in your property, the tax lien is paid (in part or in whole depending on the equity) out of the sales proceeds at the time of closing. If the home is being sold for less than the lien amount, the taxpayer can request the IRS discharge the lien to allow for the completion of the sale.

What does release of federal lien mean?

When you pay off your full tax balance or when the IRS runs out of time to collect the balance, the IRS will automatically release your tax lien. This removes the lien from your property. If the lien isn’t automatically released, you can write to the IRS to request the release certificate.

Can a private lender hold a lien on your property?

Your private lender will hold a lien on your property and have the legal right to demand full payment on the outstanding balance if you fall behind in making payments.

What happens when you get a loan from a friend?

Federal tax deductions. As with a loan from a bank, private loans allow you, if you itemize on your income taxes, to benefit from the federal tax deduction for home loan interest paid. Whether it’s a relative or a friend, your private lender stands to gain in a number of ways, such as: Achieving a better rate of return.

Can a family and friend loan be foreclosed on?

Trying to combine a family-and-friend loan with a traditional bank loan can lead to the bank refusing to go forward, if you appear to be taking on more debt than you can handle.) Your private lender can even foreclose if you default on the loan.

What does the law say about loaning money to friends and relatives?

The statute of frauds mandates that certain agreements must be in writing or they are unenforceable. As a result, a handshake agreement with a friend or relative that is not in writing could lead to an inability to legally enforce the agreement for repayment. Another consideration is the tax consequence of a loan.