What does a favorable labor efficiency variance indicate?

Olivia House

Olivia House

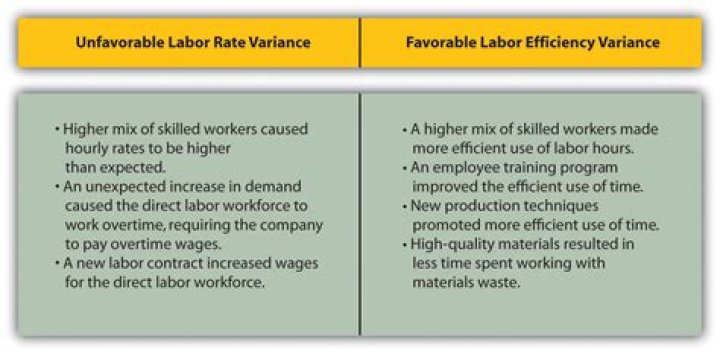

A favorable labor efficiency variance indicates better productivity of direct labor during a period. Causes for favorable labor efficiency variance may include: Hiring of more higher skilled labor (this may adversely impact labor rate variance).

What does a favorable direct materials price variance mean?

A favorable DM price variance occurs when the actual price paid for raw materials is less than the estimated standard price. It could mean that the firm’s purchasing department was able to negotiate or find materials with lower cost.

What does a favorable direct materials cost variance indicate quizlet?

A favorable direct materials price variance indicates which of the following? The standard cost of materials purchased was greater than the actual cost of materials purchased.

What does direct material variance indicate?

The direct material variance is the difference between the standard cost of materials resulting from production activities and the actual costs incurred. This is the difference between the standard and actual number of units used in the production process, multiplied by the standard cost per unit.

Which department is often responsible for the direct materials price variance?

As it is the responsibility of the purchasing department to get the materials at best price of the company, purchasing department would be held responsible for this variance.

What are the causes of price variance?

Here are several possible causes of a direct material price variance:

- Discount application. A discount is to be retroactively applied to the base-level purchase price at the end of the year by the supplier, based on actual purchase volumes.

- Materials shortage.

- New supplier.

- Rush basis.

- Volume assumption.

What is overhead cost variance?

Overhead variance refers to the difference between actual overhead and applied overhead. You can only compute overhead variance after you know the actual overhead costs for the period. The difference between the actual overhead costs and the applied overhead costs are called the overhead variance.

When standard manufacturing costs are recorded in the accounts and the cost variances are immaterial?

When standard manufacturing costs are recorded in the accounts and the cost variances are immaterial at the end of the accounting period, the cost variances should be: A) Carried forward to the next accounting period. B) Allocated between cost of goods sold, finished goods, and goods in process.