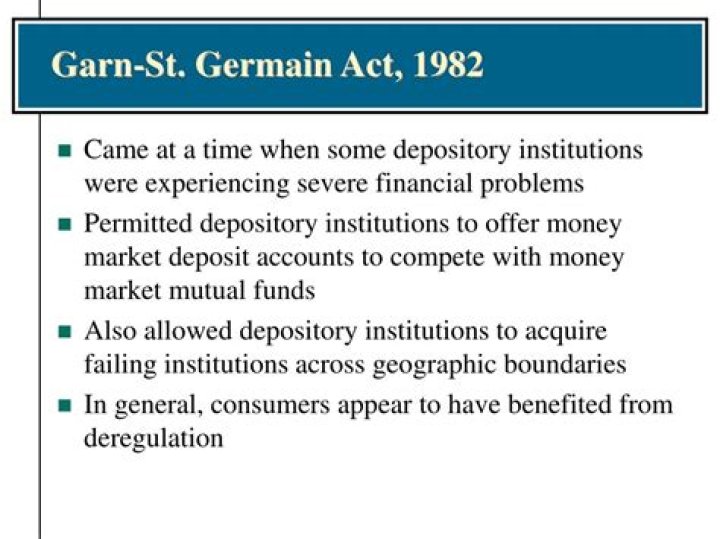

What did the Garn-St Germain Depository Act of 1982 do?

Rachel Acosta

Rachel Acosta

The Garn–St Germain Depository Institutions Act of 1982 ( Pub. L. 97–320, H.R. 6267, enacted October 15, 1982) is an Act of Congress that deregulated savings and loan associations and allowed banks to provide adjustable-rate mortgage loans.

Who is a relative for purposes of the Garn-St Germain Act?

The Garn-St. Germain Act provides certain rights and protections to a surviving spouse, a surviving joint tenant, a surviving tenant by the entirety, and a relative who inherits, when property with an existing loan or mortgage (other than a reverse mortgage) is transferred.

Does my mortgage have a due on sale clause?

Do all mortgages have a due-on-sale clause?: Although the majority of mortgages contain due-on-sale clauses, there are still some mortgages that are assumable. Such mortgages include VA, FHA and USDA loans. Even though these types of loans are assumable, prospective buyers must still qualify for the loan.

What is an alienation clause in a loan?

In real estate, an alienation clause, or due-on-sale clause, refers to contract language that requires the borrower to pay the full mortgage balance, as well as accrued interest, back to the lender before they can transfer the property to a new buyer.

What is the Garn-St Germain Act of 1982?

The Garn-St Germain Act aimed to ease the pressures on banks, thrifts, and their insurance funds. The act expanded previous deregulation of deposit rates by creating a new money market deposit account (MMDA) for households that proved to be very popular.

Which level of regulation the Garn-St Germain Depository Institutions Act was?

At the same time, Fed Regulation Q restricted banks and savings and loans (known as S&L or thrifts) from raising their deposit interest rates. Title VIII of the Garn-St. Germain Depository Act, “Alternative Mortgage Transactions,” authorized banks to offer adjustable-rate mortgages.

Can my bank call my mortgage?

Yes, under specific circumstances a lender can demand repayment even if your loan service is current. On term and intermediate loans, as well as mortgages, there is usually language in the note that allows a lender to call the note if the lender deems himself insecure.

Do banks enforce due-on-sale clause?

Mortgages with due-on-sale clauses are not assumable. That means the buyer of your property cannot take over your current mortgage. However, if someone inherits your property and plans to live in it, your bank or mortgage lender cannot enforce the due-on-sale clause.

What type of loan allows the interest rate to fluctuate depending on money market conditions?

Variable rate loans are loans that have an interest rate that will fluctuate over time in line with prevailing interest rates. They generally have lower starting interest rates than fixed rate loans, but the interest rate and payment amounts can change over time. Sometimes they are also known as floating rate loans.

What is the prepayment clause?

A prepayment penalty clause states that a penalty will be assessed if the borrower significantly pays down or pays off the mortgage, usually within the first five years of the loan. Prepayment penalties serve as protection for lenders against losing interest income.

What do you need to know about the Garn St Germain Act?

The due-on-sale clause permits lenders to foreclose on a current loan or property when it is transferred to someone else. The act enabled the use of trusts to pass property to heirs and minors. When a relative inherits and occupies a residence, the Garn-St. Germain Act bans the lender from enforcing the due-on-sale clause.

Who are the sponsors of the Garn St.Germain Depository Institutions Act?

The Garn-St. Germain Depository Institutions Act was named after sponsors Congressman Fernand St. Germain, a Democrat from Rhode Island, and Senator Jake Garn, a Republican from Utah. Co-sponsors of the bill included Congressman Steny Hoyer and Senator Charles Schumer.

Why is a second mortgage unenforceable under Garn-St Germain?

But the Garn-St. Germain Law says such a clause is unenforceable. The reason is that placing a second loan against the property makes the first loan safer, not less secure. If the borrower doesn’t pay the first mortgage, the second mortgage lender will usually step in to keep the payments current to avoid being wiped out by foreclosure.