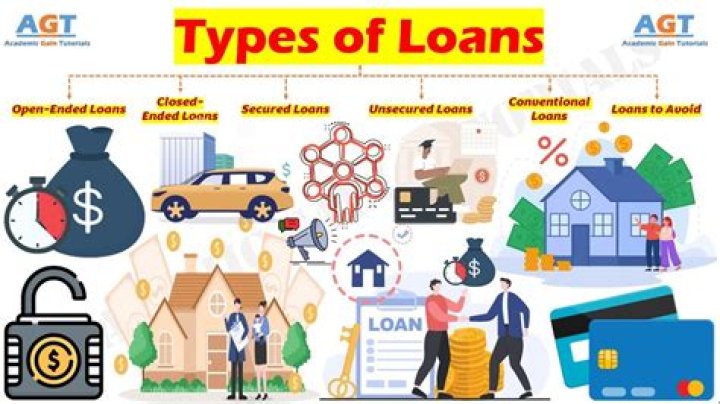

On which type of loan is interest never tax deductible?

Isabella Ramos

Isabella Ramos

personal loans

Interest paid on personal loans is not tax deductible. If you borrow to buy a car for personal use or to cover other personal expenses, the interest you pay on that loan does not reduce your tax liability. Similarly, interest paid on credit card balances is also generally not tax deductible.

Is interest on personal loan tax deductible?

Section 24(b) of the Income Tax Act, 1961, allows for a tax rebate on personal loan if the amount is used for home renovation or improvement. In this case, interest paid on personal loan repayment up to Rs. 30,000 can be claimed as deduction from the total taxable income. 2 lakh is allowed for the interest paid.

What are the rules for tax deductions for interest?

But tax rules on deductibility can be confusing. Business interest is treated differently than other types of interest. For example, personal interest (other than home mortgage interest and some interest on student loan debt) is not deductible. Investment interest is only deductible to the extent of net investment income each year.

Is the interest on a home loan deductible?

In order to be deductible, interest must be defined as deductible in the Internal Revenue Code. For example, interest that you pay on your home is defined as mortgage interest. Interest that you pay on funds used to purchase investment assets would be deductible as investment interest.

When do you deduct interest on a line of credit?

The interest expense when you borrow money, either through your margin account, an investment loan or a line of credit, and use it for the purpose of earning investment income is generally tax deductible. This tax deduction is important since it can dramatically reduce your true, effective after-tax cost of borrowing.

When is interest paid on a loan nondeductible?

The law says that interest paid on a loan secured by your account balance is nondeductible if any of the account balance used to secure the loan is attributable to elective deferrals that you made. Well heck, that’s why you signed up for a 401 (k) or 403 (b) plan — to elect to defer part of your wages into the plan.