Is FDIC by account or bank?

Mia Horton

Mia Horton

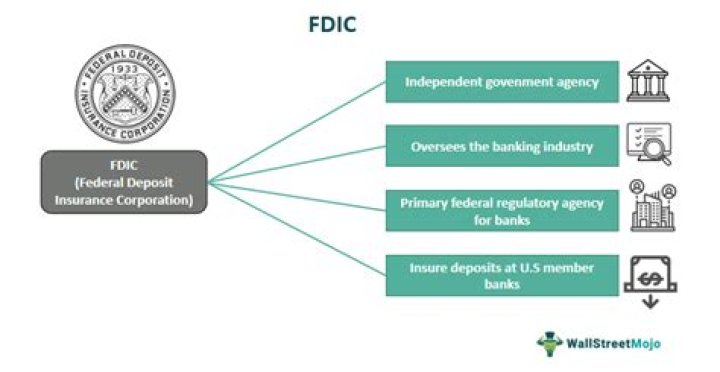

FDIC insurance covers depositors’ accounts at each insured bank, dollar-for-dollar, including principal and any accrued interest through the date of the insured bank’s closing, up to the insurance limit.

Can your identity be stolen from a bank statement?

Criminals can steal your identity in a number of ways, for example finding your credit card or bank statements in your rubbish or stealing your driving licence or bank cards from your purse or wallet.

What accounts are not covered by FDIC?

FDIC does not insure nondeposit investment products, even if they were purchased from an insured bank, including:

- annuities.

- mutual funds.

- stocks.

- bonds.

- government securities.

- municipal securities.

- U.S. Treasury securities.

What if a bank is not FDIC?

Accounts That Aren’t Insured Some banks may offer financial products that aren’t FDIC insured. Examples include stock market trading accounts, stocks and bonds and insurance policies. Money market funds, which are investment products you can put money into through a brokerage, are generally not FDIC-insured.

Do I have to have money to open a bank account?

Most banks don’t require much to open one. Most online banks don’t have a minimum initial deposit. Even if you don’t need very much money to open a bank account, watch out for monthly minimum balance requirements. Some banks may charge you a service fee if your balance falls below their minimum balance amount.

How much does the FDIC cover for identity theft?

The FDIC is a deposit insurance program backed by the federal government that protects bank depositors for up to $250,000. The FDIC, however, does not cover instances of identity theft and the financial losses that may accompany it.

What do financial institutions need to do about identity theft?

Each financial institution or creditor that offers or maintains one or more covered accounts must develop and implement a written Identity Theft Prevention Program (Program) that is designed to detect, prevent, and mitigate identity theft in connection with the opening of a covered account or any existing covered account.

How are covered accounts determined by the FDIC?

Each financial institution must periodically determine whether it offers or maintains covered accounts. As part of this determination, the financial institution must conduct a risk assessment to determine whether it offers or maintains covered accounts taking into consideration c. its previous experiences with identity theft.

What happens to my FDIC insurance if my bank fails?

If the sale doesn’t happen, the FDIC will send you a check for the insured portion of your qualifying accounts. If the FDIC needs further input from you, you’ll receive correspondence in the mail. In most cases, bank failures are brief and uneventful for customers.