How is deferred revenue recorded?

Matthew Wilson

Matthew Wilson

What Is Deferred Revenue?

- Deferred revenue is a liability on a company’s balance sheet that represents a prepayment by its customers for goods or services that have yet to be delivered.

- Deferred revenue is recognized as earned revenue on the income statement as the good or service is delivered to the customer.

How the deferred revenue expenditure is treated in the books of accounts *?

Such expenses are taken to Profit and loss Account in part every year and thus unwritten off portion may be allowed to stand in the balance sheet on the asset side.

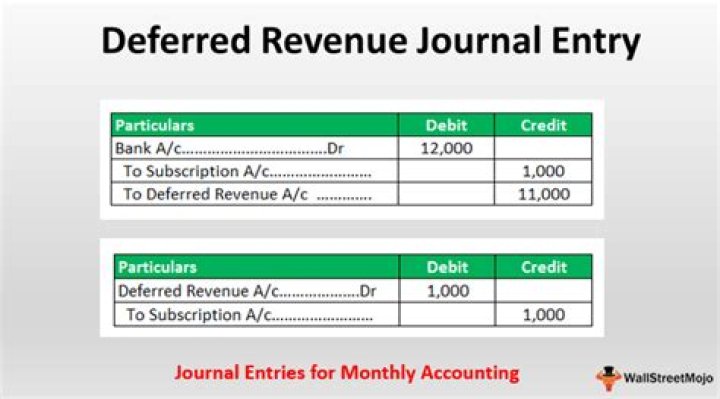

What is deferred revenue journal entry?

The following Deferred Revenue Journal Entry provides an outline of the most common journal entries in Accounting. In simple terms, Deferred Revenue. read more means the revenue that has not yet been earned by the Products/Services are delivered to the Customer and is receivable from the same.

What are the examples of deferred revenue expenditure?

For example, the cost of raw materials, labour expenses, depreciation on assets, etc. However, there is also one more category of expenses, often referred to as Deferred Revenue Expenditure. These expenses are revenue in nature but the business derives benefits from these expenses for a period of more than one year.

Is high deferred revenue good?

Deferred revenue is considered a liability because the revenue recognition or earnings process is not yet complete, and a company’s goods or services are still due to the buyer or customer. A good example of the type of company that would have high levels of deferred revenue is a magazine subscription service.

Accounting for Deferred Revenue Since deferred revenues are not considered revenue until they are earned, they are not reported on the income statement. Instead they are reported on the balance sheet as a liability. As the income is earned, the liability is decreased and recognized as income.

Is deferred sales revenue an asset?

You will record deferred revenue on your business balance sheet as a liability, not an asset. Receiving a payment is normally considered an asset.

Can you record deferred revenue before receiving cash?

Accrued income is income that a company will recognize and record in its journal entries when it has been earned – but before cash payment hast been received. This deferred income is accrued revenue (income).

What happens to deferred revenue in an acquisition?

consequences to the buyer of assuming a deferred revenue liability in a taxable asset acquisition of a business. Although the recommendations in this report are limited to the tax treatment of the buyer, the report discusses the tax treatment of both the buyer and the seller in these transactions. Deferred revenue is a type of liability.

Is the Deferred revenue a liability or an asset?

Yes, deferred revenue is a liability and not an asset. The payment the company gets represents something owed to the customer. All companies selling products or providing services that require prepayments deal with deferred revenue. Here are some examples: Let’s dive deeper into the last example.

When do you recognize deferred revenue in accrual accounting?

Deferred Revenue (also called Unearned Revenue) is generated when a company receives payment for goods and/or services that it has not yet earned. In accrual accounting, revenue is only recognized when it is earned. If a customer pays for good/services in advance, the company does not record any revenue on its income…

Can a deferred revenue payment be treated as gross income?

In Rev. Rul. 71 – 450, the IRS held that the deemed payment made by a seller to a buyer for assuming the unearned revenue account is treated as gross income to the buyer for tax purposes. Presumably, the buyer can defer the income recognition if it uses the accrual method.