How does the cost volume profit model accommodate non linear costs and revenues?

Robert Guerrero

Robert Guerrero

24. How does the cost-volume-profit model accommodate non-linear costs and revenues? Non-linear costs and revenues are ignored by the model.

What does cost volume profit tell you?

Cost-volume-price (CVP) analysis is a way to find out how changes in variable and fixed costs affect a firm’s profit. Companies can use CVP to see how many units they need to sell to break even (cover all costs) or reach a certain minimum profit margin.

What are the components of cost volume profit CVP analysis?

A CVP analysis consists of five basic components that include: volume or level of activity, unit selling price, variable cost per unit, total fixed cost, and sales mix. Cost-volume-profit (CVP) analysis is used to determine how changes in costs and volume affect a company’s operating income and net income.

How do you calculate cost volume profit?

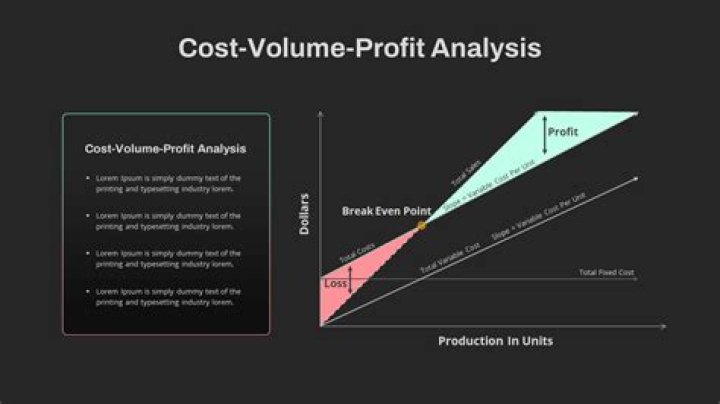

The previos equation reads: Required dollar sales for targeted profit equals fixed costs dollar plus targeted profit dollar, divided by Contribution Margin percentage. The break-even point is reached when total costs and total revenues are equal, generating no gain or loss (Operating Income of $0).

What are the three elements of cost volume profit analysis?

Classmate #1: The cost-volume profit analysis requires three vital elements to make an accurate result. Those elements are activity level, variable cost per unit, and the total fixed cost.

Which of the following is an assumption of cost-volume-profit CVP analysis?

Answer- The following is an assumption of CVP analysis = the behavior of costs and revenues are linear within the relevant range. Explanation- Cost-volume profit analysis is based on the assumption of the behavior of costs (ie- Both variable & fixed costs) and revenues are linear within the relevant range of activity.

What are the assumptions of cost-volume-profit CVP analysis?

Assumptions made in cost-volume-profit analysis To summarize, the most important assumptions underlying CVP analysis are: Selling price, variable cost per unit, and total fixed costs remain constant through the relevant range.

Why is cost-volume-profit important?

By breaking down costs into fixed versus variable, CVP analysis gives companies strong insight into the profitability of their products or services. Many companies and accounting professionals use cost-volume-profit analysis to make informed decisions about the products or services they sell.

What is the main limitation of CVP analysis?

Limitations of CVP Fixed costs not always fixed. Proportionate relation between variable cost and volume of output not always effective. Unit selling price not always constant. Not suitable for a multiproduct firm.

What are the components of cost volume profit?

The cost-volume-profit formula is:

- selling price−variable costs−fixed costs=profit.

- sales−variable expenses=contribution margin.

- profit=sales−variable expenses−fixed expenses.

What are the basic components of cost volume profit CVP analysis?

What is cost volume profit CVP analysis and how is it used in decision making?

A cost volume profit definition, defined also as the CVP model, is a financial model that shows how changes in sales volume, prices, and costs will affect profits. Use the CVP analysis for planning, making projections, and for decision-making purposes. A CVP model can be used to calculate a breakeven sales volume.

The components of cost volume profit analysis

- Activity level. This is the total number of units sold in the measurement period.

- Price per unit. This is the average price per unit sold, including any sales discounts and allowances that may reduce the gross price.

- Variable cost per unit.

- Total fixed cost.

What are the assumptions of cost volume profit CVP analysis?

Here are some assumptions about the use of CVP analysis in business. CVP analysis costs can be segregated into fixed and variable portions and total fixed costs remain constant at all output levels. In CVP, cost linearity is preserved over the relevant range, and revenues are constant per unit.

What to look for in a cost Volume Profit Analysis?

In cost-volume-profit analysis –or CVP analysis, for short – we are looking at the effect of three variables on one variable: Profit. CVP analysis estimates how much changes in a company’s costs, both fixed and variable, sales volume, and price, affect a company’s profit.

Which is the simple model for revenue and costs?

The simple model for revenue is revenue= quantity∗price. r e v e n u e = q u a n t i t y ∗ p r i c e.

How are variable costs related to unit costs?

Variable costs are tied to the amount you produce or sell. They might include raw material for a manufacturer or the cost of goods for someone in sales. For our simplified model we assume that variable costs are proportional to quantity. This makes our cost function linear. For our simplified model variable costs= unit costs*quantity.

When are non-manufacturing costs recorded as expenses?

B. Expenses are incurred when assets are used to generate revenue. C. Manufacturing-related costs are initially recorded as expenses. D. Non-manufacturing costs should be expensed in the period in which they are incurred. C. Manufacturing-related costs are initially recorded as expenses. 16.