How do you shop with different mortgages?

David Mack

David Mack

Shopping for Mortgage Rates

- Get Your Credit Score. Credit scores help lenders determine who qualifies for loans, and the interest rates they’ll pay.

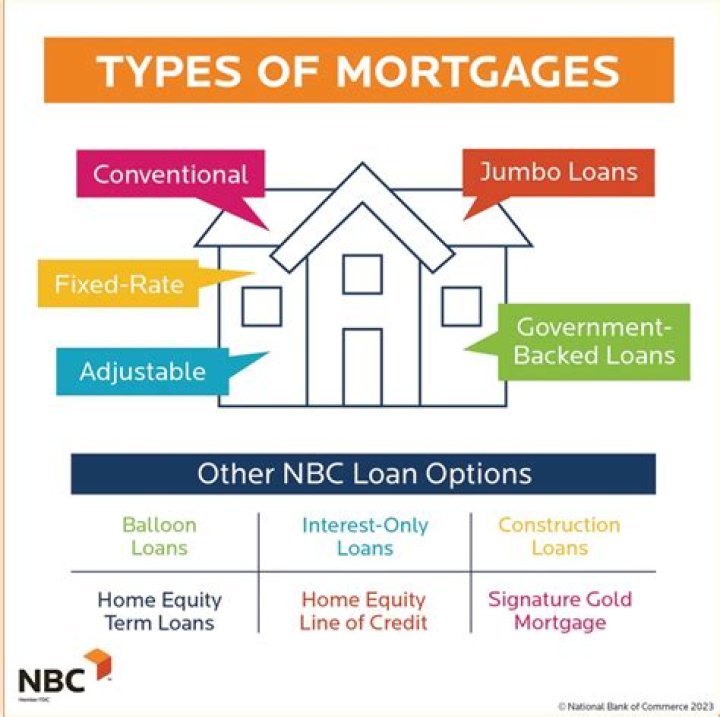

- Consider Mortgage Types.

- Review Financing Options.

- Contact Several Lenders.

- Add in the Additional Costs.

- Negotiate.

- Get It in Writing.

- Picking the Best Rate.

Why should a person shop around with different lenders?

But it’s not the only reason it pays to shop around. By comparing lenders, you’ll see variations in lender origination fees, points, mortgage insurance premiums and third-party fees. You’ll also get a sense of how long it takes lenders to close a loan, how well they communicate and their customer service philosophies.

Do you need to shop around for mortgage lenders?

You’ll have a mortgage payment for 15, 20 or 30 years, so it’s smart to shop around to find the best mortgage lenders out there. Get preapproved for your mortgage. Boost your chances of having your offer accepted by getting preapproved. Compare rates from several mortgage lenders.

Is it OK to shop around for a mortgage broker?

It never hurts to shop around on your own to see if your broker is really offering you a great deal. As mentioned earlier, using a mortgage calculator is an easy way to fact check if your broker is offering you a good deal.

Do all mortgage brokers have access to the same deals?

‘ Some brokers do check lenders’ direct-only deals too. However, they are more likely to charge a fee. In reality, it’s unlikely a broker could guarantee you access to EVERY mortgage, as exclusive deals can be arranged between lenders and brokers (and clubs that brokers can join).

Does pulling your credit for a mortgage hurt your score?

All new auto or mortgage loan or utility inquiries will show on your credit report; however, only one of the inquiries within a specified window of time will impact your credit score. All inquiries will likely affect your credit score for those types of loans.

What are three benefits to using money saved or invested instead of credit?

3 benefits of using money saved or invested instead of credit? no contract, no interest or fees, not spending future income. loan which the borrower must repay the amount in a specified number of equal payments. may combine elements of closed and open end credit.

How long does pre approval last?

The time a mortgage preapproval is valid before expiring can vary depending on your lender. But in most cases, it lasts for around 60 – 90 days. Your financial situation can change substantially within a few months.

Does shopping for a mortgage hurt credit?

You can shop around for a mortgage and it will not hurt your credit. The impact on your credit is the same no matter how many lenders you consult, as long as the last credit check is within 45 days of the first credit check.

How to shop for a mortgage and compare mortgage rates?

So by all means, organize your quotes by mortgage rate with the lowest on top. But remember — rates aren’t the only thing to consider. Your loan estimates will list other costs and fees that you need to take a close look at before choosing a mortgage lender. To do this, look carefully at the Loan Estimate you get from each lender.

What happens if you don’t shop around for a mortgage?

Failing to shop for a mortgage could cost you. Consumers who consider interest rates offered by multiple lenders or brokers may see substantial differences in the rates. For example, our research showed that a borrower taking out a 30-year fixed rate conventional loan could get rates that vary by more than half a percent.

How to shop around for a home loan?

Make sure you know what you can afford and how much of a down payment you have. Obtain and compare loans (or pre-approval quotes) from potential lenders and talk to them too, as the posted rates are often negotiable. Ask at least three lenders for the same loan amount, loan term and type of loan so you can compare the information.

Can you open another line of credit while shopping for a mortgage?

Don’t open other lines of credit while you are trying to take out a mortgage. In fact, applying for a credit card or auto loan while you are shopping for a mortgage is far riskier than ignoring the 45-day window for rate shopping, Ulzheimer says.