Does bad debt expense lower accounts receivable?

Rachel Acosta

Rachel Acosta

Bad debt expenses are generally classified as a sales and general administrative expense and are found on the income statement. Recognizing bad debts leads to an offsetting reduction to accounts receivable on the balance sheet—though businesses retain the right to collect funds should the circumstances change.

What happens when bad debt expense is recorded?

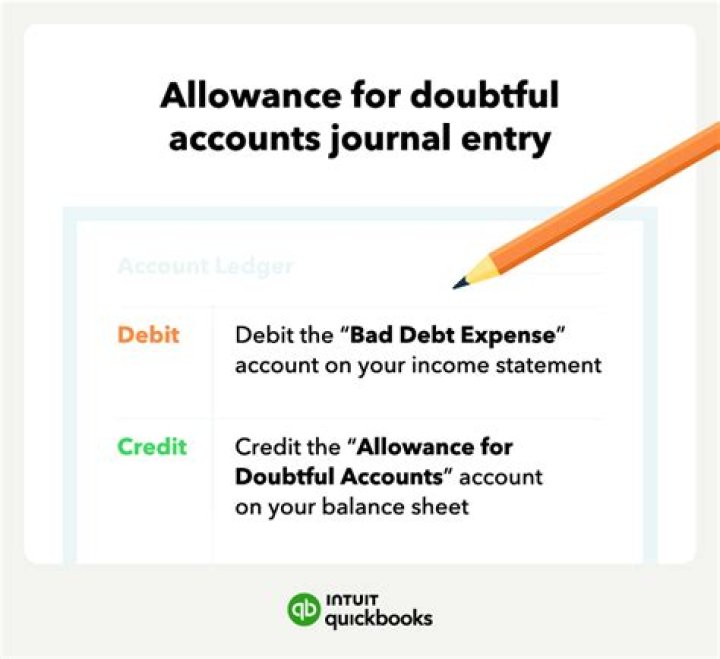

When sales transactions are recorded, a related amount of bad debt expense is also recorded, on the theory that the approximate amount of bad debt can be determined based on historical outcomes. This is recorded as a debit to the bad debt expense account and a credit to the allowance for doubtful accounts.

Does bad debt expense increase accounts receivable?

Under the direct write-off method, bad debt expense serves as a direct loss from uncollectibles, which ultimately goes against revenues, lowering your net income. While it is arrived at through. For example, in one accounting period, a company can experience large increases in their receivables account.

Where is bad debts shown in final accounts?

Irrecoverable debts are also referred to as ‘bad debts’ and an adjustment to two figures is needed. The amount goes into the statement of profit or loss as an expense and is deducted from the receivables figure in the statement of financial position.

How do you record adjusting entry for bad debt expense?

Increase the bad debt expense account with a debit and decrease the accounts receivable account with a credit. For example, if customer Lucy has a 91-day late $125 invoice, your bad debt expense journal entry would look like this: Bad Debts Expense – Debit $125. Accounts Receivable – Credit $125.

When does a receivable become a bad debt expense?

A bad debt expense is recognized when a receivable is no longer collectible because a customer is unable to fulfill their obligation to pay an outstanding debt due to bankruptcy or other financial problems.

How is bad debt expense recorded in a journal?

Estimate uncollectible receivables. Record the journal entry by debiting bad debt expense and crediting allowance for doubtful accounts. Allowance for Doubtful Accounts The allowance for doubtful accounts is a contra-asset account that is associated with accounts receivable and serves to reflect the true value of accounts receivable.

Where does bad debt expense go on a balance sheet?

A company will debit bad debts expense and credit this allowance. The allowance for doubtful accounts is a contra-asset account within accounts receivable, which means that it reduces the loan receivable account when both balances are listed in the balance sheet.

How does the aging of accounts receivable determine bad?

Focusing on the past due accounts receivable will assist you in estimating how much of the accounts receivable will never be collected. The estimated amount of accounts receivable that will never be collected should be the credit balance in the general ledger account Allowance for Doubtful Accounts.