Do you get reimbursed for tax deductions?

Andrew Mccoy

Andrew Mccoy

Description:Tax deductions reduce your Adjusted Gross Income or AGI and thus your taxable income on your income tax return. This can cause your tax refund to increase, the taxes you owe to decrease, or make you tax balanced – no refund or owed taxes.

Can I write off a related party loan?

Generally, a loss on a loan is deductible, as either a capital loss or a business investment loss, only if the loan was made to earn income. The same principles apply to payments made to honour a loan guarantee. For the payment to create a deductible loss, there must be a guarantee fee.

How do you calculate mileage for taxes?

Once you have determined your business mileage for the year, simply multiply that figure by the Standard Mileage rate. For tax year 2020, the Standard Mileage rate is 57.5 cents/mile. Carrying through the example above: 5,000 business miles x $0.575 standard rate = $2,875 Standard Mileage deduction.

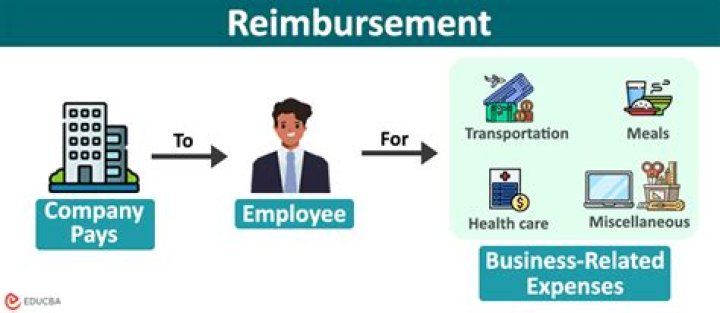

Is the reimbursement of tax advice a taxable benefit?

Is the reimbursement of tax advice a taxable benefit? No. The Canada Revenue Agency has confirmed that reimbursements made because of the employer’s error are not considered as a taxable benefit or as income.

How are loss allowances divided on a tax return?

The legislation implicitly appears to require us to divide the deductions allowance between various types of loss carried forward. Specifically, we are required to state on the company’s tax return how much of the deductions allowance is to be allocated to certain types of loss.

What is the tax deduction for carried forward losses?

The company has a ‘deductions allowance’ of £5 million (CTA 2010 s 269ZW). This is the amount of profit that against which carried forward losses can be set off without restriction. If the companies accounting period is less than 12 months, the £5 million allowance is reduced accordingly.

What is the loss restriction in CTA 2010 part 7za?

The intention of the loss restriction that is now in CTA 2010 Part 7ZA is to restrict the loss relief available to companies with profits over £5 million so that the total loss relief is restricted to £5 million plus half the profits above that number. What does it mean to me?