Do I need to file Form 8990?

Olivia House

Olivia House

A pass-through entity allocating excess taxable income or excess business interest income to its owners (that is, a pass-through entity that is not a small business taxpayer) must file Form 8990, regardless of whether it has any interest expense.

Can Form 8990 be E filed?

Although TaxAct does not support IRS Form 8990, you can still prepare and e-file your return in TaxAct. You will need to attach Form 8990 to your return in the Filing steps if you answer no on the Schedule B – Excess Business Interest Expense screen (Schedule B – Business Interest Expense in TaxAct 1065 Edition).

What is the 163 J limitation?

Limitation of Business Interest Expense In general, the purpose of IRC Section 163(j) is to limit a taxpayer’s deduction for business interest expense (“BIE”) in any tax year to the sum of: The taxpayer’s business interest income for the tax year; 30% of the taxpayer’s ATI for the tax year (but not less than zero).

How does 163 J apply?

Section 163(j) in general Section 163(j) generally may apply to any taxpayer. It generally limits a taxpayer’s business interest deductions for a taxable year to the sum of: (1) 30% of the taxpayer’s adjusted taxable income (ATI) for that year, (2) its business interest income and (3) floor plan financing interest.

What is the purpose of Form 8990?

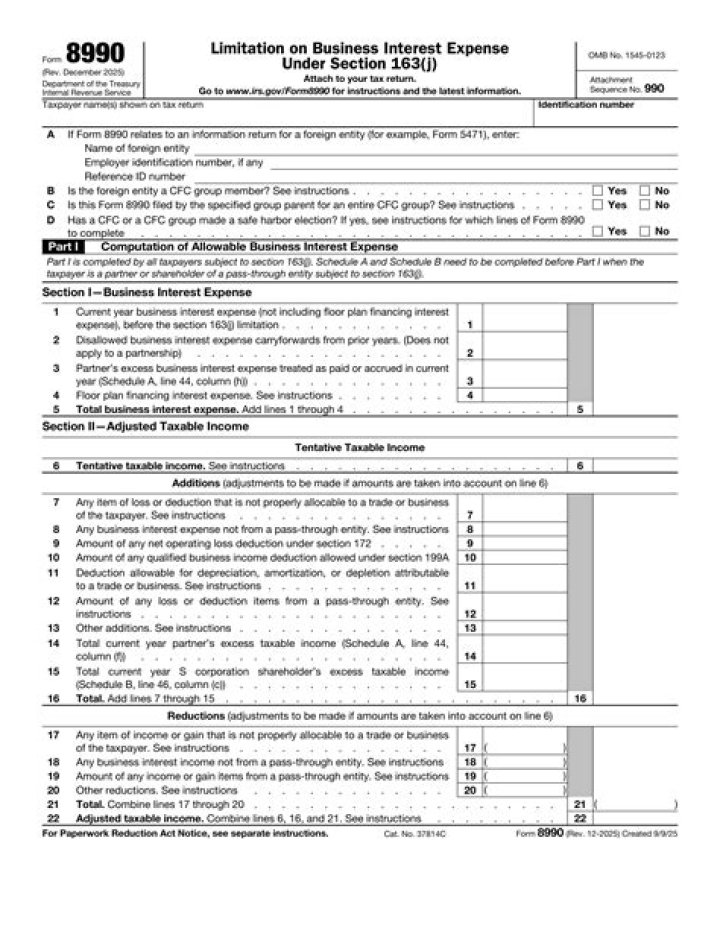

Use Form 8990 to calculate the amount of business interest expense you can deduct and the amount to carry forward to the next year.

What is the business interest limitation?

The section 163(j) limitation is applied at the partnership level. As provided in Q/A 1, the amount of deductible business interest expense in a taxable year cannot exceed the sum of the partnership’s business interest income, 30% of the partnership’s ATI, and the partnership’s floor plan financing interest expense.

What is a section 163 J adjustment?

Under Sec. 163(j)(1), a taxpayer’s deduction for interest is limited to the sum of (1) the taxpayer’s business interest income for the tax year; (2) 30% of the taxpayer’s adjusted taxable income for the tax year; and (3) the taxpayer’s floor plan financing interest expense for the tax year (in sum, the Sec.

Who is subject to the 163j limitation?

Who is subject to the section 163(j) limitation? A2. For tax years beginning after 2017, the limitation applies to all taxpayers who have business interest expense, other than certain small businesses that meet the gross receipts test in section 448(c) (“exempt small business”) (see Q/A 3-4).

Are 163 J regulations final?

Like the 2020 Proposed Regulations, the 2021 Final Regulations provide that a RIC shareholder that receives a section 163(j) interest dividend may treat the dividend as interest income for purposes of section 163(j), subject to holding period requirements and other limitations.

When do I need to attach Form 8990?

You will need to attach Form 8990 to your return in the Filing steps if you answer no on the Schedule B – Excess Business Interest Expense screen (Schedule B – Business Interest Expense in TaxAct 1065 Edition). If you answer no on this screen, you will be prompted to attach a PDF version of Form 8990 using Attachment Manager .

What is the IRS Form 8990 business interest carryforward?

A taxpayer who is a U.S. shareholder of an applicable controlled foreign corporation (CFC) that has business interest expense, ha a disallowed business interest expense carryforward, or is part of a CFC group election generally, must attach Form 8990 with Form 5471, Information Return of U.S. Persons With Respect To Certain Foreign Corporations.

How is adjusted taxable income calculated on form 8990?

(Form 8990, Section I, lines 1-5) A taxpayer’s adjusted taxable income is taxable income, computed as though all of the business interest expense is otherwise allowable business interest expense and taking into account all other applicable limitations (e.g., the at-risk limitation), with certain additions and reductions.

How to report partnership income on form 8893?

The draft instructions to Form 8893 refer partnerships to the instructions for Form 1065, U.S. Return of Partnership Income, for how to report these amounts to the partners. … Part III—S corporation pass-through items. This part is only completed by S corporations that are subject to Code Sec. 163 (j).