Can you get a mortgage with 583 credit score?

Robert Guerrero

Robert Guerrero

The most common type of loan available to borrowers with a 583 credit score is an FHA loan. FHA loans only require that you have a 500 credit score, so with a 583 FICO, you will definitely meet the credit score requirements. We can help match you with a mortgage lender that offers FHA loans in your location.

Can I get approved with a 583 credit score?

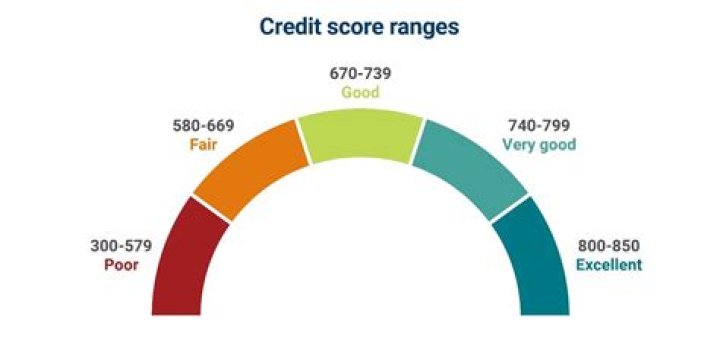

Your score falls within the range of scores, from 580 to 669, considered Fair. A 583 FICO® Score is below the average credit score. Some lenders see consumers with scores in the Fair range as having unfavorable credit, and may decline their credit applications.

Is 583 a good credit score UK?

A credit score of 721-880 is considered fair. A score of 881-960 is considered good. A credit score of 604-627 is good. A score of 628-710 is considered excellent (reference: ).

What should my FICO score be to get a mortgage?

If your three FICO scores were 700, 709, and 730, the lender would use the 709 as the basis for its decision. Reviewing this large collection of credit reports and credit scores gives the mortgage lender a more comprehensive picture of your credit risk.

Which is credit score do mortgage lenders use?

While the FICO ® 8 model is the most widely used scoring model for general lending decisions, banks use the following FICO scores when you apply for a mortgage: As you can see, each of the three main credit bureaus (Equifax, Experian and TransUnion) use a slightly different version of the industry-specific FICO Score.

What should my credit score be to get a FHA loan?

Someone with a lower credit score needs to meet the 43% limit, but if your score is on the higher side, FHA mortgage lenders may allow a ratio as high as 50%. If you apply for an unsecured personal loan, which is based on your credit, a high income or low amount of existing debt can be even more important.

When do Lenders look at your credit score?

It’s not a complete snapshot of your overall financial picture, but lenders look at it when evaluating you for credit cards, loans and mortgages. But like all things in the financial world, credit scores are nuanced. There are actually multiple versions of your credit score, and they all mean different things to lenders.