Can you capitalize research and development?

Rachel Acosta

Rachel Acosta

According to the Financial Accounting Standards Board, or FASB, generally accepted accounting principles, or GAAP, require that most research and development costs be expensed in the current period. However, companies may capitalize some software research and development, or R&D, costs.

Does R&D need to be capitalized?

One of the most surprising pay-for provisions in the TCJA is the elimination of immediate expensing of research and development (R&D) costs. The TCJA requires capitalization of all R&D costs, including software development costs incurred in tax years beginning after Dec. 31, 2021.

What does capitalizing R&D mean?

Capitalising R&D means moving some or all of the cost of your development team from above the Ebitda line to below the Ebitda line – effectively increasing the profit on which an acquirer might value the company – and taking costs that would normally be recognised on the profit and loss (P&L) statement and turning them …

Is research and development R&D an expense or an asset?

Research and development costs no longer appear as intangible assets on the balance sheet, but as expenses on the income statement.

Why are R&D expenses not capitalized?

The main reason companies aren’t allowed to capitalize their research and development costs is that there’s no way to reliably measure the future economic benefits of those costs. R&D involves trial and error – a lot of error.

What is the difference between expensing and capitalizing?

The primary difference between capitalizing and expensing costs is that you record capitalized costs on a balance sheet, and you record expensed costs on an income statement or statement of cash flows. Capitalized costs also display as investing cash outflow, while expensed costs display as operating cash outflow.

When to capitalize research and development ( are & D )?

Capitalizing R&D Expenses Guide to R&D capitalization vs R&D expense. Under the GAAP, firms are required to expense research and development (R&D) in the year they are Fixed and Variable Costs Cost is something that can be classified in several ways depending on its nature.

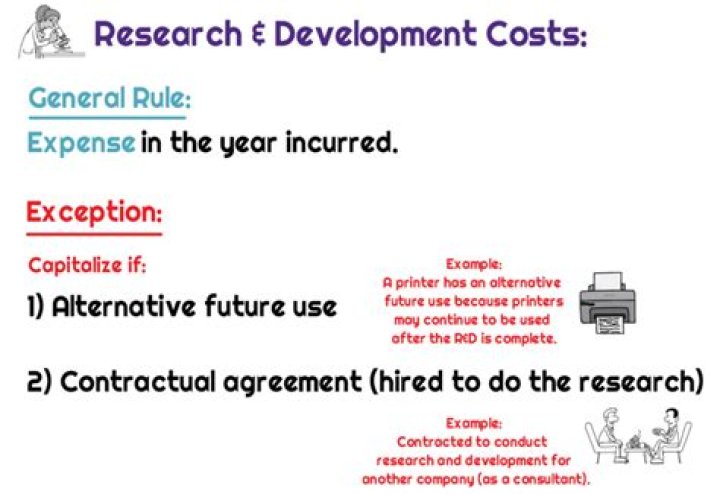

What is the general rule for research and development costs?

General rule for research and development costs Research and development costs are –> charged to expense when incurred –> because future economic benefits are uncertain Research and development (R&D) costs 1. tangible assets 2. intangible assets 3. personnel costs

When do you capitalise research and development costs in IFRS?

IFRS: Initial Recognition: Research and Development Costs Charge all research cost to expense. Development costs are capitalised only after technical and commercial feasibility of the asset for sale or use have been established.

How is research and development ( are & D ) classified under GAAP?

Under the GAAP, firms are required to expense research and development (R&D) in the year they are Fixed and Variable Costs Cost is something that can be classified in several ways depending on its nature. One of the most popular methods is classification according