Can I contribute to a Roth IRA after January 1?

Robert Guerrero

Robert Guerrero

Answer: No. Generally speaking, the IRS allows you to make your IRA contribution for a particular tax year up until April 15 of the following year. This rule applies to both traditional IRAs and Roth IRAs, giving you some flexibility in terms of the timing of your annual IRA contribution.

What happens if you contribute to a Roth IRA and you make too much money?

You must pay an excess contribution penalty equal to 6 percent of the amount you contributed to your Roth IRA when you contribute even though you’re not eligible. For example, if you contribute $5,000 when your contribution limit is zero, you’ve made an excess contribution of $5,000 and would owe a penalty of $300.

What is the deadline for contributing to a Roth IRA for 2021?

May 17

The IRS states that you can make contributions until your tax filing deadline. 5 That date for individual filers is typically April 15 but was May 17 in 2021. You are able to make contributions to your 2021 Roth IRA until April 15, 2022.

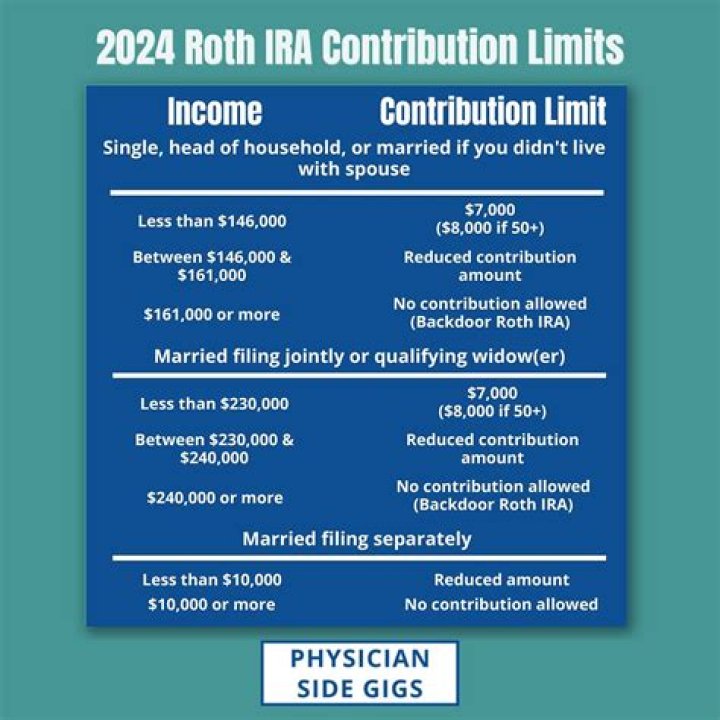

How much income is too much for Roth IRA?

To contribute to a Roth IRA in 2021, single tax filers must have a modified adjusted gross income (MAGI) of $140,000 or less, up from $139,000 in 2020. If married and filing jointly, your joint MAGI must be under $208,000 in 2021 (up from $206,000 in 2020).

What’s the maximum amount you can contribute to a Roth IRA per year?

The maximum contribution for 2018 is $5,500 (or $6,500 if you’re 50 or older by the end of the year). This dollar limit on annual contributions applies to total IRA contributions (including deemed traditional IRA and Roth IRA set up by an employer as a separate account under a qualified retirement plan).

How old do you have to be to contribute to a Roth IRA?

Anyone of any age can contribute to a Roth IRA, but the annual contribution cannot exceed their earned income. Let’s say that Henry and Henrietta, a married couple filing jointly, have modified adjusted gross income (MAGI) of $175,000.

What was the original limit for IRA contributions?

The initial limit was $1,500. Congress passes the Economic Recovery Tax Act, raising the contribution limit to $2,000 and not tying the limit to money earned at a job with a retirement plan available. Congress eliminated the universal deduction in the Tax Reform Act.

When was the first employer run IRA created?

First introduced in the Employee Retirement Income Security Act of 1974 ( better known as ERISA ), the IRA is a portable retirement account which allows contributions from workers outside of the worker’s employer. The IRA family also claims employer run IRAs; one example is the Simplified Employee Pension IRA (SEP IRA), created in 1978.