Can anyone do income-based repayment?

David Mack

David Mack

Any borrower with eligible federal student loans can make payments under this plan. This plan is the only available income-driven repayment option for parent PLUS loan borrowers.

Are income-driven repayment plans a good idea?

While income-driven repayment options can make monthly student loan payments more affordable, these programs do have some potential disadvantages. Since you’ll be repaying your loan for longer, more interest will accrue on your loans. That means you may pay more under these plans — even if you qualify for forgiveness.

What is an income-based repayment plan?

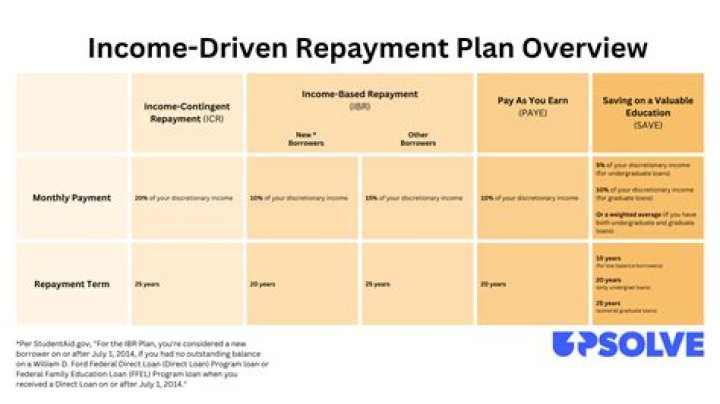

Income-Based Repayment (IBR) is a federal student loan repayment program that adjusts the amount you owe each month based on your income and family size. You are a new borrower or had no outstanding balances on a federal student loan when you received the new loan.

How long can you be on an income-driven repayment plan?

25 years

The maximum repayment period is 25 years. After 25 years, any remaining debt will be discharged (forgiven). Under current law, the amount of debt discharged is treated as taxable income, so you will have to pay income taxes 25 years from now on the amount discharged that year.

What is one disadvantage of the income-based repayment plan?

Con: Forgiven debt is taxed Under income-driven plans, taxes apply to your forgiven debt. It is understandably frustrating. The amount counts as personal income, which means it is taxed, depending on your personal financial standing, somewhere around 20%.

What is the maximum income for income-based repayment?

Just as there is no absolute income limit in IBR, there is no absolute limit on how much you can have forgiven. You can have $200,000 forgiven if that’s what you end up with at the loan forgiveness point.

What is one advantage of the income-based repayment plan?

Income-driven repayment plans base the monthly loan payment on the borrower’s income, not the amount of debt owed. This can make the loan payments more affordable if your total student loan debt is greater than your annual income.

What happens if my IBR payment is 0?

A zero calculated monthly loan payment still counts as a payment toward loan forgiveness. If the borrower persists with low or zero calculated monthly loan payments for most of the repayment term, the remaining debt will be forgiven.