Are assets covered by long-term care insurance?

Robert Guerrero

Robert Guerrero

Partnership-eligible long-term-care insurance programs, which most states now offer, allow you to keep some of your assets if you exhaust all of your benefits from an eligible long-term-care policy and have to rely on Medicaid.

Do long-term care policies have a cash value?

Pro: Permanent life insurance policies build cash value, which you can tap to cover expenses other than long-term care. Stand-alone long-term care policies don’t have cash value.

Can I add my uncle to my health insurance?

In many cases, your insurance provider will permit you to carry virtually any family member that you can claim as a dependent. Such family members might include your elderly parents, adult children and disabled relatives.

How much is long-term care insurance per month?

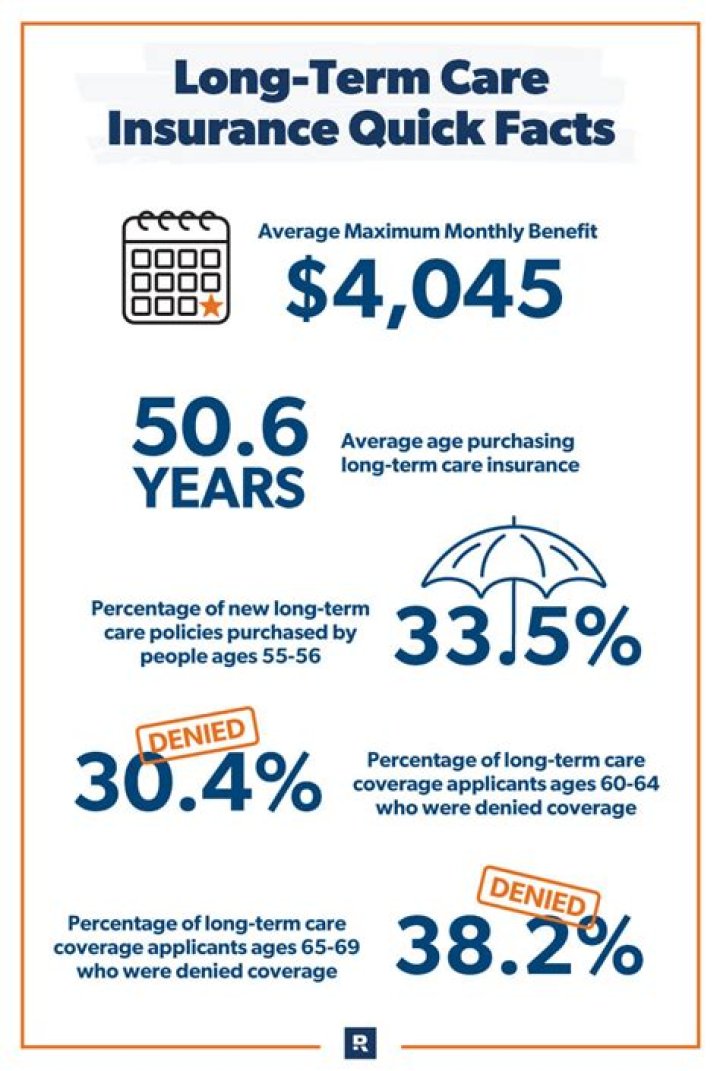

The average annual long-term care insurance premium for a 65-year-old couple is around $3,750 (or about $313 per month). As far as the payout, the typical long-term insurance policy provides a benefit of $160 per day for nursing home care for a set number of years (three is most common).

Which of the following types of care is typically not covered in a long-term care policy?

Under a Long Term Care policy, which benefit would be typically excluded or limited? “Alcohol rehabilitation”. (Addictive behavior rehabilitation is normally excluded or limited under a Long Term Care policy.)

Is long-term health care a good investment?

Consumer and financial experts generally agree that LTC insurance is a bad investment unless the monthly premium is 5% or less of your monthly income. Remember that you may never need long-term care at all, or you might not need enough care to collect much in the way of insurance benefits.

Can someone use my health insurance?

Adding Someone to Your Insurance When signing up for insurance, go over their policy about adding your household members. Though you cannot add anyone you just live with like a roommate, it is possible to add a non-dependent to your health insurance if you wish for them to receive care.

Is a spouse a dependent or beneficiary on health insurance?

A beneficiary can be a person or a legal entity that is designated by you to receive a benefit, such as life insurance. For example, if you will be including your spouse in your medical coverage and designating him or her as a recipient of your life insurance, then your spouse is both a dependent and a beneficiary.

How does assert based long term care work?

Assert based long term care insurance plans function similarly to regular whole life insurance policies or annuities, but with the added benefit of long-term care coverage. After applying for the coverage and going through underwriting, you make premium payments to the insurer.

What is asset based long term care insurance?

What is Asset-Based Long-Term Care? Asset-based long-term care (“ABLTC”) is an innovative insurance strategy that provides coverage for long-term care expenses without running the risk of “wasting” premiums if you don’t need long-term care.

Can a whole life policy be used for long term care?

The beauty of ABLTC is that, if you don’t need long-term care, the annuity or whole-life policy retains its value and pays out to your designated beneficiary. And many people who might not qualify for traditional LTCI due to preexisting conditions may still be able to obtain coverage.

Is there a cap on Long Term Care?

Long-term care riders usually have a monthly cap, expressed as a percentage of the death benefit. For instance, if a policy has a $100,000 death benefit and a 4% monthly cap, it would pay out up to $4,000 per month for long-term care expenses. The other approach is what is known as a “hybrid” plan.